How IFRS 17 will change operations

In May 2017 IASB released IFRS 17 to be effective on 1 January 2023.

This will be the biggest challenge the insurance industry has faced in a generation. The finance operating model of every insurer working within an IFRS jurisdiction will have to be re-engineered. These changes have a huge impact on how insurer’s performance is measured, especially by investors. We expect the investors to find IFRS 17 challenging, resulting in revaluation of some insurers’ market capitalisation.

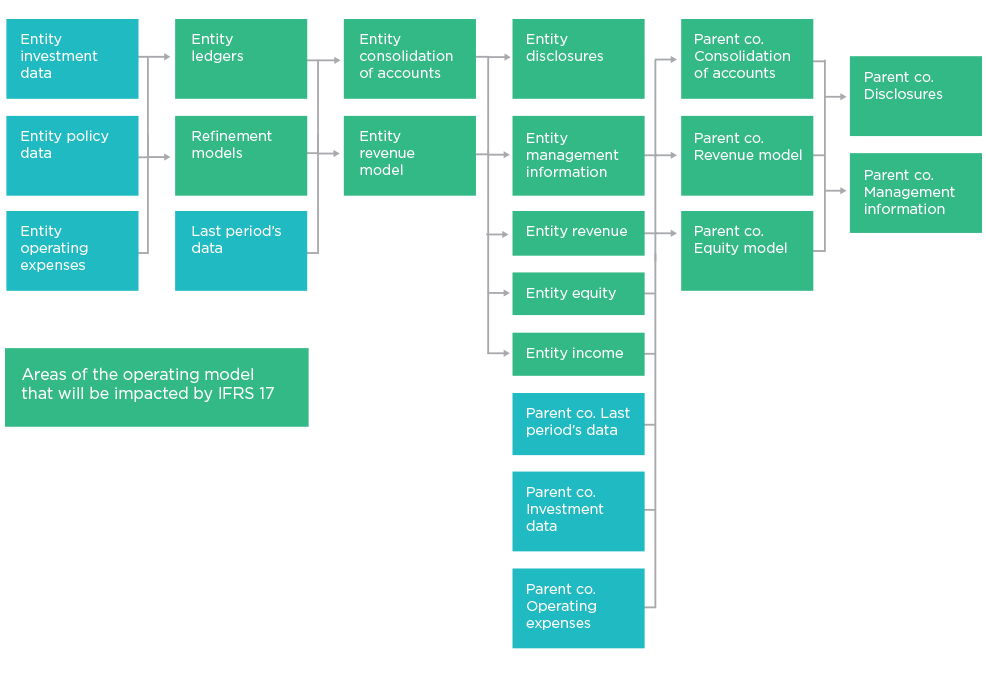

Policy categorisation will change into one of three measurement models, there will be change in loss recognition for policies and the volume and the complexity of information will significantly increase compared to today. Furthermore, valuation models will change, as will profit emergence patterns, now to be measured over a policy’s lifetime. Assumptions will change and new ones added, while disclosures and statements will have additional reporting lines leading to greater investment transparency.n short, the introduction of IFRS will mean significant changes to the process. From our IFRS 17 delivery work for insurance clients, we see key areas that will be impacted. We have indicated these in figure 1 above, whereby the boxes coloured green indicate the areas of the process that will change as a result of IFRS17.

Depending on insurers’ approach and motivation, it may be possible to work towards minimising the impact of the huge increase in operational work and cost. Essential steps such as aligning their internal accounting policies, building better operating models or increasing levels of automation may need to be taken to reduce risk and limit impact.

To ensure successful delivery and implementation, incremental resources will be required to deliver the change in a structured and coordinated manner. Resources may be limited, so smart new ways of delivering change will need to be adopted. In our experience of delivering change, the later the project is started, the less organised it will be and the more expensive it will become as insurers compete for scarce resources.

Delivery dates are fixed, the quality is non-negotiable, which leaves investment cost versus operational cost as the only variable.

Ultimately IFRS 17 marks an opportunity for insurers to work smarter – but first companies may need to actively embrace and deliver the change. Who will be proactive and who will struggle to implement change? Perhaps only time will tell. As a partner for change, we are working to support insurance businesses through the IFRS 17 period – and we’ll also be keeping a close eye as things develop.

Partners